InsurTech Trends: Top 5 Insurance Technology Trends for 2019

Top-notch Insurance technology trends to ride the herd in 2019

The world is changing fast with increasing technological advancements like digitization. This is leading to major shifts in all sectors of business. These changes aim at simplifying the whole product purchase life cycle and making the services smarter, cheaper and more convenient. In the insurance sector, the introduction of new technologies in the year 2019 is expected to benefit the insurer, as well as insurers.

Let us watch over the 5 top-notch trends of the InsurTech industry.

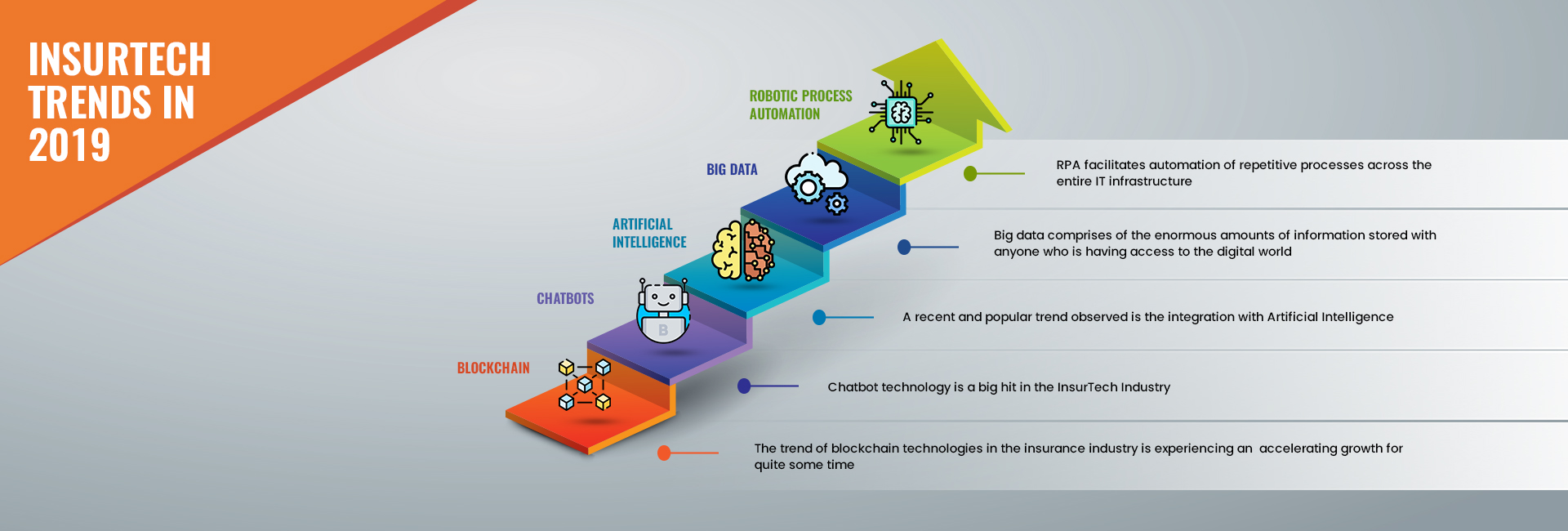

- Robotic Process Automation (RPA)

- Artificial Intelligence (AI)

- Chatbots will be in the limelight

- Big Data

- Blockchain

1. Robotic Process Automation (RPA):

RPA will become the most widely accepted insurance technology trend globally in 2019. Market research shows that the RPA market which was worth 443 million USD in 2017 is likely to accelerate to 1224 million USD by the end of 2021.

As a result, a multitude of InsurTech companies is shifting to RPA to ensure superior automation of their operations and workflows. RPA is one of the insurance industry’s biggest technology-based opportunities for 2019 and beyond. How? RPA facilitates the automation of repetitive processes across the entire IT infrastructure. This can help the insurance companies issue policies quite efficiently in very less time. Moreover, RPA can also eliminate hassles from the otherwise complex insurance cancellation process.

2. Artificial Intelligence (AI):

As the world becomes digital, insurance companies are investing in researching upon and integrating more technologically effective ways to make their customer’s life hassle-free. A recent and popular trend observed is the integration with Artificial Intelligence. The year 2019 will see more InsurTech companies complementing a considerable part of their decision-making with respect to structured data with AI data analytics and decision-making.

Therefore, RPA and AI together will increase productivity, better compliance, improved accuracy, and shortened cycle times.

3. Chatbots will be in the limelight:

Chatbot Technology was a big hit in the InsurTech industry in the year 2017-18. The survey report of the Global Trends Study for 2017 reveals that $124 million per insurer on an average is invested in the Insurance industry using Chatbot technology. One of the reasons being that chatbots can easily store the customer’s geographical and social data for customized interactions. Additional benefits with chatbots include a shortened waiting time, hassle-free claim settlements, and seamless customer support. As a result, a good number of insurance companies have already begun investing their resources in this technology to facilitate personalized insurance coverage.

Another survey by Credence Research shows that the acceptance and demand for the chatbot technology will increase exponentially by the year 2023. Looking at such high rates of the popularity of chatbot technology, the demand of technology worldwide will grow up to 5 times of what it was in 2017-18 by the year 2019.

Can be Increased Flexibility with On-demand Insurances?

The year 2019 and beyond will observe an increasing rise in on-demand insurance products that will focus on fulfilling the expectations of the modern-day tech-savvy customers. The millennial population (which will make up the largest percentage of the new customers) will go for products and services that offer flexible contacts, thereby better matching their fast-changing lifestyles.

Standard and typical insurance products come with fixed coverage and for a defined period. As a result, these do match the expectations of the millennial generation customers. What will be the trend that will satisfy the expectations of the newer generation? The first step is introducing and offering modular, flexible and on-demand insurance products. Such products will provide them the freedom to select the coverage that the customer will need.

To increase the flexibility further, on-off functionalities are being introduced and implemented to provide time flexibility. This kind of customized business models will be a great step in the 21st century, not only bringing back the control in the hands of the customers but also offering smooth customer experience. These on-demand insurance products ensure that the insurer is insured when needed and not for irrelevant coverage. The customer also gets the freedom to live life the way they want. This helps the insurer deliver services that are customer-centric, making the relationship between the insurer and the policyholder strong, positive and trustworthy.

4. Big Data:

What is Big Data? Big data comprises of the enormous amounts of information stored having access to the digital world. This data can include both structured and unstructured data. Structured data is one that is entered in defined fields and tables. Whereas, unstructured data includes social media posts, multimedia, and written reports. Unstructured data makes the most of the freely available data, however, its collection and usage are open to question.

What kind of data do insurance companies collect and how do they handle it? Typically, insurers use structured data to store their customer information and get an understanding of calculating risk, identify opportunities for their product sales and investigate fraud. Big data’s effect on the InsurTech industry regulates what level of granularity is favorable or not for their customers. This discussion is currently under analysis. Until this discussion reaches a concurrence, most of the big data can be used freely for most of the purposes.

5. Blockchain:

The trend of blockchain technologies in the insurance industry is experiencing accelerating growth for quite some time. The year 2019 will see an even bigger jump in the already prevailing trend. This technology will become frequent with the rise in fraudulent insurance claims and an increased requirement for a reliable software, and encrypted data storage mechanisms.

Blockchain technology will come as a solution to one of the major issues in the InsurTech industry i.e. the need for cooperation and coordination among the different players of the insurance industry. This issue when left unaddressed can result in an increased level of human error. Gradually, we will witness the technology being implemented in detecting fraud claims, managing policies, and safe transmission of sensitive data.

As we move ahead in the year 2019, the InsurTech companies will rapidly comeback with increased visibility across the industry. Thereafter, these companies will expand their scope to target at becoming a complete insurance value chain from just service providers. With the demand of digital consumers, corresponding technologies will integrate and work together to open the doors for this long-awaited change.